June was busting out all over until the technology stocks had a rather grim Friday on June 5th. The downdraft for semiconductors and the tech-heavy Nasdaq was ugly, and the search for answers was immediate.

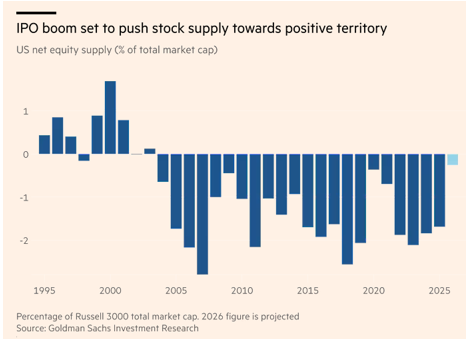

The first scapegoat was a strong payrolls number, so strong it surprised the market and the prognosticators that were all looking for a lower number. Revisions also came in higher, and that bit of good news for the labor market promptly shifted expectations: the Fed's next move is now seen as more likely a hike than a cut. Add to that the flood of equity and capital raises, both from established names and companies rushing to go public, and the up-and-to-the-right juggernaut came to a screeching halt.

Good news on payrolls, in normal parlance, would be just that. But markets read it as the kind of good news they don't like: a sign the Fed will at minimum stay on hold, and at worst, as the Bloomberg World Interest rate Probability (or WIRP) screen shows projected to deliver one hike before year-end 2026.

None of this should come as a great surprise, given that inflation has been running hotter on energy and the still-unresolved Strait of Hormuz situation. Energy has a way of bleeding into general price levels, yet somehow it still seems to be catching people off guard. And bleed it has, with CPI showing a 4.2% reading, in line with consensus.

Cutting rates won't fix a supply shock and could make it worse, which puts the doves in a genuinely tough spot. Similarly, hiking rates is unlikely to dent demand for oil and fertilizer. The high prices themselves are already doing that work.

Prior to Thursday, June 4th, one could be forgiven for feeling it was a bit like Groundhog Day: markets drifting higher despite an Iranian resolution perpetually just around the corner.

Broadcom's slight forward disappointment didn't stop the market in its tracks, but it did put a scare into the Kospi, which had stretched quite high on the backs of Korean memory names like SK Hynix. We use "disappointment" loosely as growing revenues of 48% in a single quarter is nothing to sneeze at, especially as the numbers get bigger. But that's precisely the rub: any cautionary forward stance qualifies as a miss when expectations are this elevated, even with full-year guidance intact.

The iShares Semiconductor ETF plunged 10% on Friday June 5th which was its worst single day in more than six years, before bouncing back nearly 6% on Monday. The Kospi ended Friday's session down 5.54%, with SK Hynix dropping nearly 10%.

There have also been a couple of private credit announcements worth noting, conspicuous mostly because they haven't garnered much attention. The problem with illiquid securities is that nobody worries about the illiquidity until they do, and when everyone heads for the exit at once, it tends to be disorderly. This issue surfaced a couple of months ago but was overshadowed by the Iranian conflict. It appears to still be live, with some well-known fund names gating redemptions. A canary? Hard to say, but it does add to a growing list of concerns as markets take a breather after an extraordinary run since the end of March.

In the near term, expect more volatility as investors try to square these competing forces. The enthusiasm for AI and now space is real and enormous the question becomes: is there enough room in investor's wallets to absorb all of the equity these companies are looking to raise over the summer? We may start getting answers in June, as further inflation data lands alongside a storm of mega IPOs.

The information in this commentary has been obtained from sources believed to be reliable, but its accuracy and completeness are not guaranteed. The opinions, estimates and projections constitute the judgment of Alpine Saxon Woods and are subject to change without notice. This commentary is for information purposes only and is not intended as an offer, recommendation or solicitation for the sale of any financial product or service or as a determination that any investment strategy is suitable for a specific investor. Investors should seek financial advice regarding the suitability of any investment strategy based on the investor’s objectives, financial situation and particular needs. The investments or investment strategies discussed herein may not be suitable for every investor. There is no assurance that any investment strategy will be successful.