TRADITIONAL STRATEGIES

Alpine Saxon Woods Capital Return Long Short Strategy

FUND LITERATURE

Investment Strategy Overview

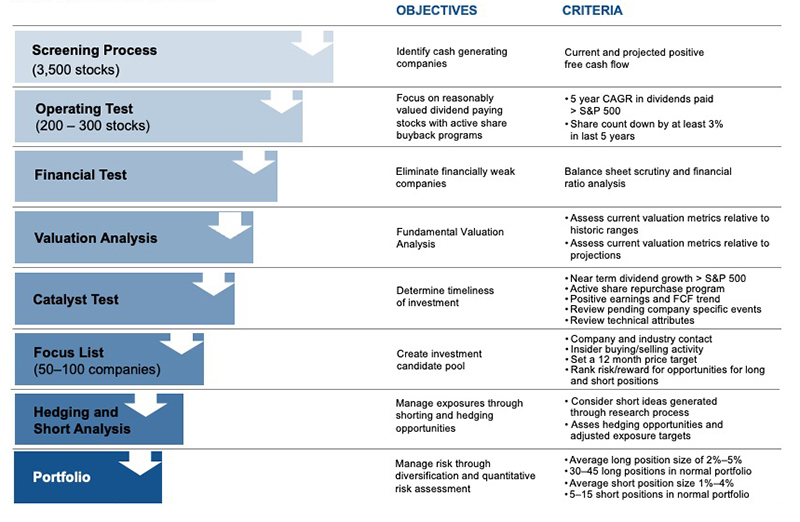

- We have reengineered the typical equity income and dividend growth approach to a more complete “return of capital” strategy.

- We look for companies that actively return excess capital to shareholders, whether it is in the form of growth in dividends or share repurchases.

- Historical analysis of owning stocks that not only raise their dividends at a greater than market rate but also buy back stock has been a value-adding strategy.

- We concentrate not only on free cash flow, return on capital, valuation and current yield, but dividends and share repurchases that have a history of being increased.

- We look for companies that have the ability to grow operating earnings and free cash flow that can allow them to increase dividends as well as buy back their shares without compromising their balance sheets. This offers investors not only the potential for growth in earnings, but an opportunity for better inflation adjusted “real return” on their income.

- Provides a defined investment process that seeks to identify sound financial companies that have a) historically paid healthy dividends with a history of, and a propensity to, raise them, and b) have a history of meaningful share repurchase programs and the propensity to continue them.

- Multi-cap style with the potential to provide a combination of capital appreciation and dividend income.

Investment Process

Portfolio Construction Parameters

- Stocks with liquidity

- Normal position size 2% to 5%

- Normal number of holdings 40 to 75

- Limit security concentration to no more than 10%

- Limit sector exposure: typically 25% or 1.5x the benchmark, whichever is greater

- Typically fully invested

- Review quantitative risk management statistics in order to know where and in what form risk exists

Portfolio Construction - Hedging

- We use various hedging instruments to help protect long exposure against downside risk and volatility.

- Attractiveness determinants include:

- Negative correlation

- Assumed risk comfort level

- Time horizon

- Cost

- Instruments include:

- Shorting individual stocks

- Shorting sector and/or market-based ETFs

- Put option contracts on individual stocks snd ETFs

Risk Management

- Position Review

- Review investment thesis if stock declines 15% from initial purchase price

- Sell Discipline

- Change in fundamentals

- No longer meets capital return parameters

- Original investment thesis has changed

- Catalysts no longer exist

- Operating health deterioration

- Financial health deterioration

- Valuation

- Stock reaches valuation target

- Diversification

- Individual security limits

- Sector limits

Meet the Team

No items found.

No items found.

No items found.

No items found.

More Strategies & Investments

Traditional Strategies

The information contained on this website is the property of Alpine Saxon Woods LLC (“ASW”) and is being provided for information purposes only. This website and the information contained herein is not an offer to sell or the solicitation of an offer to buy any securities or instruments, or a recommendation, representation of suitability or endorsement of any security or investment. Since ASW cannot anticipate all the requisites of each individual viewer, there is no consideration given for the specific investment needs, objectives or tolerances of any of the viewers. ASW’s services are provided to a limited number of private investment funds whose offerings are made only pursuant to a confidential private placement memorandum and related subscription documents as well as private wealth management and separately managed accounts. Before making any investment decision, individuals should consult their own advisors, including legal and tax advisors.