Dividend Strategy Commentary

Market & Economic Review

Equity markets opened the year with a measure of stability as investors weighed the scale of AI infrastructure spending against the timing and frequency of Federal Reserve rate cuts. This equilibrium shifted abruptly as a regime change in Venezuela and the escalation of conflict in the Middle East forced a rapid repricing of geopolitical risk and energy market volatility. With the West Texas Intermediate (WTI) oil price climbing to a peak of nearly $120 per barrel in the quarter, the impact on economic growth and profit dramatically shifted the analysis of how negative an impact higher prices would have on global demand and margins. We thought there might be some early-year volatility, but so far, better economic data and an unexpected shift in the geopolitical landscape have seemed to be taken in stride by investors. We do not think anyone had a change in leadership in Venezuela on their 2026 bingo cards, but the reaction by investors suggests that getting a new government regime in charge of the world’s largest oil stockpiles is a net positive, at least at first glance. Where this goes as more detail emerges is not as clear.

The prevailing optimism driven by a robust technology capex cycle and tailwinds from last year’s fiscal legislation initially pointed toward above-trend economic for 2026. This consensus is now being tested and double-digit earnings growth expectations for the S&P 500 for the year are facing greater scrutiny. Management commentary during 1Q26 earnings calls will be critical in assessing how these disruptions impact operations, demand and full-year guidance.

Dividend SMA Product Review

Major contributors

Data center real estate investment trust (REIT) Equinix (EQIX) was a major contributor to the strategy this quarter. The provider of data center capacity and services for enterprise, network and cloud providers continued to benefit from demand and pricing power driven by the data center needs of AI computing. Precious metals miner Agnico Eagle Mining (AEM) was a major contributor to the strategy this quarter. Gold and other metals continued solid gains through the end of the year and into January when metal prices took a breather and retreated somewhat. Mining stocks performed well in the quarter overall despite the volatility. The Williams Companies (WMB), one of the largest energy infrastructure companies in North America, was a major contributor to the strategy this quarter. Its network of pipelines, natural gas processing facilities, natural gas liquids (NGL) fractionation facilities, and storage greatly benefitted from the surge in energy prices in the quarter.

Major detractors

Broadcom (AVGO) was sold off by investors as concerns about both its software division (derived from the VMWare acquisition several years ago) and its position in the semiconductor space. Companies that have benefited from the AI-related trade in general underperformed in the quarter as investors began to have concerns about the levels of capex and the macro picture. Shares of Prudential Financial (PRU) detracted from the strategy’s performance for the quarter after reporting allegations of misconduct at its Prudential of Japan subsidiary. The company voluntarily suspended sales at the division for 90 days pending an investigation. Seeing as its Japan operations are a major contributor to the overall company’s financial performance and the uncertainty of the situation; we exited the position in the quarter. Shares of global banking company JP Morgan (JPM) were a detractor to the strategy’s performance for the quarter as financial stocks in general suffered from a spike in interest rates brought on by global inflation fears and worries about a slowing economy impacting loan growth and credit quality.

Current industry/sector overweights/underweights

At the end of 1Q26, the Dividend SMA was positioned with its largest overweights versus its benchmark (SDY) in technology, led by positions in Broadcom (AVGO), Texas Instruments (TXN), Cisco (CSCO) and new addition Qualcomm (QCOM). These names have solid exposure to growth in their respective end markets including AI spending and deployment, and security. Other sector overweights included Financials with healthy dividend payers JP Morgan (JPM), US Bancorp (USB) and Bank of America (BAC) benefitting from loan growth and investment banking and trading profitability. The strategy was also overweighted in Materials with domestic steel providers Reliance Steel (RS) and Steel Dynamics (STLD)both benefitting from tariff policy punishing imports, as well as gold miner Agnico Eagle Mining (AEM) helped by precious metals prices.

The strategy’s largest sector underweights included the Industrials sector where the potential for slower GDP growth has us somewhat cautious, the Utility sector where higher interest rates are typically a poor backdrop for the stocks, and communication services where finding healthy dividend payers has proved elusive.

Market & Economic Outlook

The Federal Reserve finds itself in a precarious position. While geopolitical tension exerts upward pressure on energy-driven inflation, cooling labor markets and a housing sector burdened by 6.5% mortgage rates signal a need for restraint. We believe current hawkish rate forecasts are overextended; central banks are unlikely to tighten aggressively against a backdrop of equity market stress and softening private credit sentiment. This environment should support a stable dollar and provide a constructive tailwind for U.S. large caps and dividend payers.

While we remain somewhat cautious, we will continue to look for exceptional opportunities to purchase stocks that have characteristics that include inflation protected income streams that include healthy dividend payments, pricing power to offset cost pressures, limited impact or even benefits from a trade war, and as always, growing free cash flow that allows company managements to continue to invest in their businesses and pay dividends.

While we cannot know for certain what the remainder of 2026 will bring, we will maintain our focus on our investment strategy. We continue to monitor the global economic situation as we move through global changes in trade, monetary policy, and the political and economic turbulence that an aggressive Russia, conflict in the Middle East, and military action in Venezuela has brought to an already challenging geopolitical backdrop. The outlook for the economy is fraught with question marks and there will be many winners and many losers. We will always strive to manage that ebb and flow in the Alpine Saxon Woods Dividend SMA strategy by continuing to seek those stocks that pay a healthy dividend to shareholders and have the financial strength to continue to do so in the future.

Alpine Saxon Woods, LLC is an independent asset management firm with investment advisory services provided by Alpine Woods Capital Investors LLC and Saxon Woods Advisors, LLC (collectively Alpine Saxon Woods). Alpine Woods Capital Investors LLC and Saxon Woods Advisors, LLC are investment advisers registered with the Securities & Exchange Commission. The information in this commentary has been obtained from sources believed to be reliable, but its accuracy and completeness are not guaranteed. The opinions, estimates and projections constitute the judgment of Alpine Saxon Woods and are subject to change without notice. This commentary is for information purposes only and is not intended as an offer, recommendation or solicitation for the sale of any financial product or service or as a determination that any investment strategy is suitable for a specific investor. Investors should seek financial advice regarding the suitability of any investment strategy based on the investor’s objectives, financial situation and particular needs. The positions described represent holdings as of the date reported and are subject to change without notice. Reported positions do not include all securities that were purchased, sold or held in client accounts over time. It should not be assumed that holdings are or will be profitable or that securities purchased in the future will be profitable or will equal the performance of the securities in this list. References to specific securities do not represent a recommendation to purchase or sell any particular security outside a managed account. SDY, the State Street SPDR S&P Dividend ETF, tracks the performance of the S&P High Yield Dividend Aristocrats Index and is provided as a benchmark to illustrate a strategy targeting a comparable investment universe. ETF fees and expenses are lower (e.g., 0.10% – 0.35% expense ratios being common) than is typical for a managed account (up to 1% managed directly and up to 3% in a wrap There is no assurance that any investment strategy will be successful.

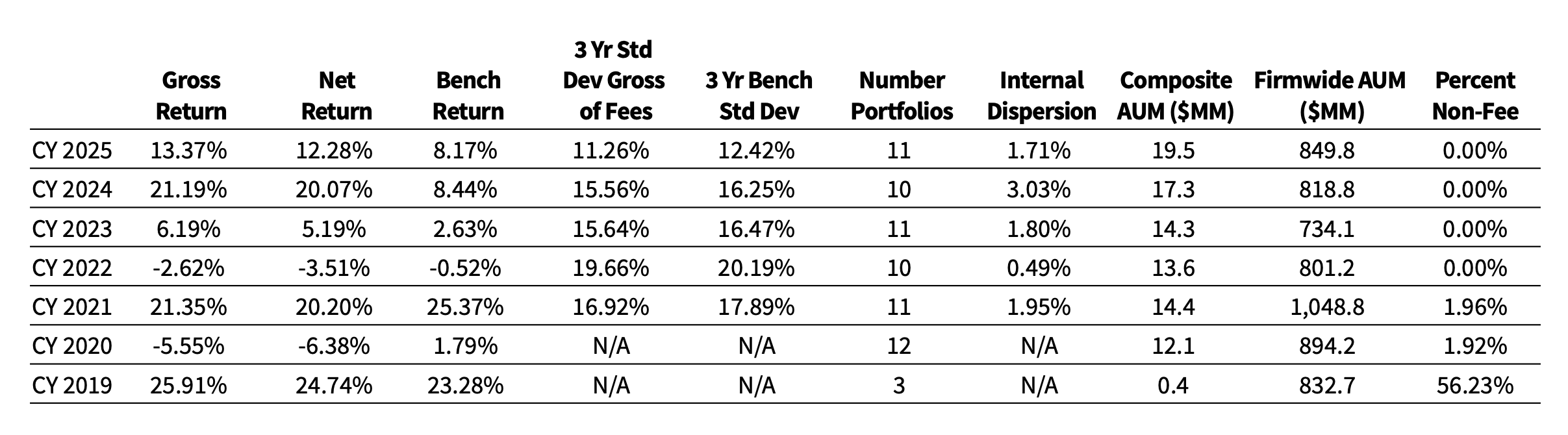

PERFORMANCE (AS OF 3/31/26)

COMPOSITE TIME-WEIGHTED RETURN REPORT

Dividend

Alpine Saxon Woods, LLC claims compliance with the Global Investment Performance Standards (GIPS®) and has prepared and presented this report in compliance with the GIPS standards. Alpine Saxon Woods, LLC has been independently verified for the periods January 1, 2019, through December 31, 2025.

A firm that claims compliance with the GIPS standards must establish policies and procedures for complying with all the applicable requirements of the GIPS standards. Verification provides assurance on whether the firm’s policies and procedures related to composite and pooled fund maintenance, as well as the calculation, presentation, and distribution of performance, have been designed in compliance with the GIPS standards and have been implemented on a firm-wide basis. The Dividend composite has had a performance examination for periods beginning January 1, 2019, through December 31, 2025.

GIPS® is a registered trademark of CFA Institute. The CFA Institute does not endorse or promote this organization, nor does it warrant the accuracy or quality of the content contained herein.

Alpine Saxon Woods, LLC is an independent asset management firm established in 2022 and based in Purchase, NY. The firm history begins in 2019 with the predecessor firm, Alpine Woods L.P. Alpine Saxon Woods is the parent company of two registered investment advisors, Alpine Woods Capital Investors LLC and Saxon Woods Advisors, LLC. The firm takes a thematic and tailored approach to investing, with a focus on underappreciated growth.

Composite Inception Date: 11/1/18 Composite Creation Date: 10/10/18

Composite Description: The Dividend strategy invests in companies that have maintained or increased dividends for at least the past 5 years. Fundamental research is performed on each company’s ability to sustain its dividend and potentially increase those payments in the future, incorporating analysis on free cash flow potential and numerous balance sheet metrics. The strategy is market capitalization and sector agnostic, but the nature of dividend paying companies tends to tilt towards a mid-to-large capitalization profile.

The composite uses the SPDR S&P Dividend ETF (SDY). The SDY tracks the performance of the S&P High Yield Dividend Aristocrats Index.

Internal dispersion is calculated as the equal-weighted standard deviation of annual gross returns for those portfolios that were included in the composite for the entire year.

Fees include management fee and transaction fees only. The management fee is 1%.

AVAILABLE UPON REQUEST: List of composite descriptions Policies for valuing investments, calculating performance and preparing GIPS reports

From inception through 9/30/23, the composite used monthly dollar weighted returns, adjusting for capital inflows and outflows through Eze Investor Accounting (formerly Penny-It-Works). From 10/1/23 to 12/31/2025, the composite uses daily time-weighted returns from Orion Advisor Technology LLC, which measures performance as a percent of capital at work on each trading day and links them together to produce a return for a stated period.

Results prior to June 30, 2022, are from a predecessor firm, Alpine Woods LP.

Past Performance Does Not Guarantee Future Results

Quick Facts

As of

March 31, 2026

Fund

SMA Inception Date

1/1/2009

Benchmark

S&P Dividend ETF

Strategy AUM

$51.25M

Vehicles Available

Separate Account

Investment Minimum

Negotiable

Fees

Negotiable

The information contained on this website is the property of Alpine Saxon Woods LLC (“ASW”) and is being provided for information purposes only. This website and the information contained herein is not an offer to sell or the solicitation of an offer to buy any securities or instruments, or a recommendation, representation of suitability or endorsement of any security or investment. Since ASW cannot anticipate all the requisites of each individual viewer, there is no consideration given for the specific investment needs, objectives or tolerances of any of the viewers. ASW’s services are provided to a limited number of private investment funds whose offerings are made only pursuant to a confidential private placement memorandum and related subscription documents as well as private wealth management and separately managed accounts. Before making any investment decision, individuals should consult their own advisors, including legal and tax advisors.